I'm Beau Eckstein, your Business Ownership Coach | Investor Financing Podcast host. In this post I walk you through the practical, step-by-step process of acquiring a business using SBA financing — from the first conversation with a seller to signing the loan documents and closing the deal. If you've found a business you want to buy and you're wondering what documents you need, how lenders evaluate a transaction, or how long the process takes, this guide will give you a clear, actionable roadmap.

What to gather from the seller: the documents that matter most

The single most important thing you can do early in seller conversations is ask for documentation. For SBA loans we underwrite off tax returns, so the primary items you need from the seller are:

- Three years of business tax returns (e.g., 2021, 2022, 2023)

- Year-to-date interim financial statements

- Current balance sheet (if available)

These documents allow lenders to “spread” the financials, meaning they review and normalize past performance rather than relying on a single year-to-date snapshot. Getting these early helps you and prospective lenders quickly evaluate whether the cash flow of the existing business can support the new SBA debt payment.

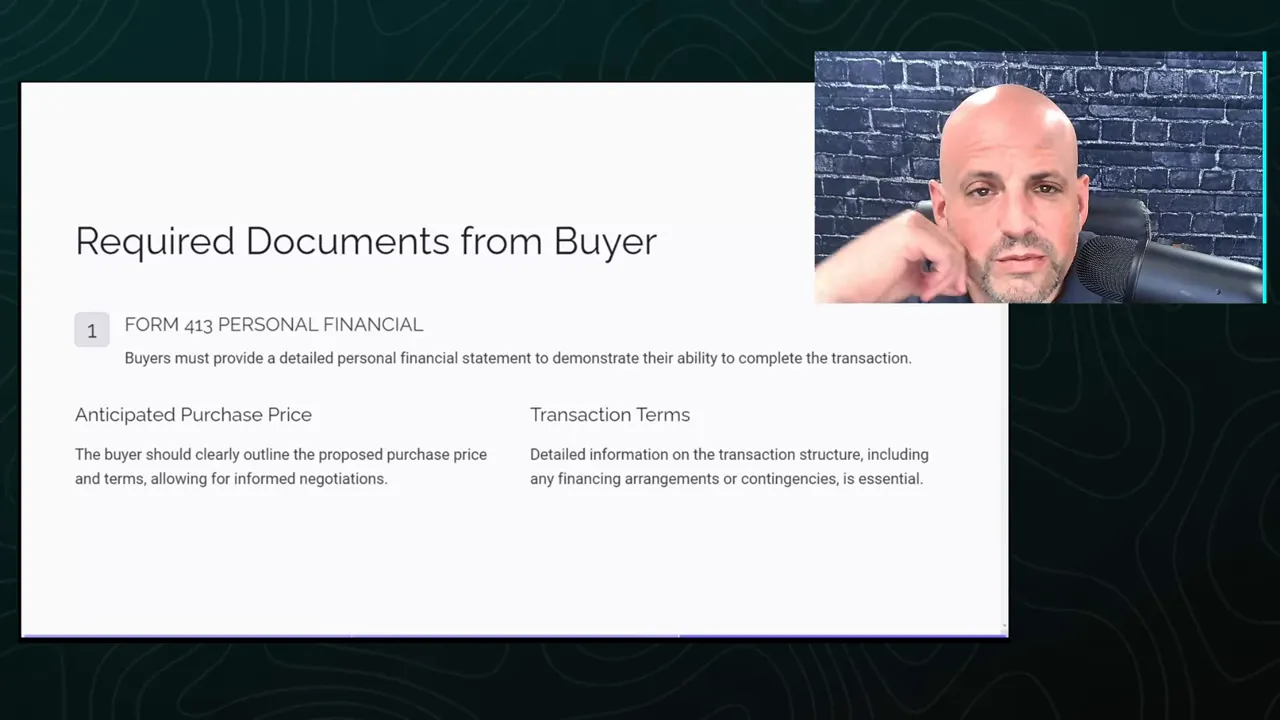

What lenders need from you: the buyer's checklist

Photo by Giorgio Tomassetti on Unsplash

On the buyer side, lenders typically ask for:

- Anticipated purchase price and proposed terms

- Form 413 (SBA Personal Financial Statement) — you can Google it or some banks have their own forms

- A resume or bio that explains relevant business or management experience

- Three years of personal tax returns (and a 2023 W-2/paystub if applicable)

Putting these together quickly improves your chances of getting an early term sheet. In many cases, this initial package is enough for lenders to perform a preliminary analysis and issue a conditional term sheet — not a loan commitment, but a crucial step forward.

Initial analysis and the term sheet: what it means

Photo by Sebastian Herrmann on Unsplash

A term sheet is where lenders tell you the deal looks probable. During this stage lenders:

- Verify basic eligibility

- Spread and normalize the business financials (not relying solely on year-to-date numbers)

- Calculate coverage ratios and determine if the business cash flow supports the new debt

For business acquisitions using an SBA 7(a) loan, one crucial metric is the debt service coverage ratio (DSCR). A DSCR greater than 1.15 is typically required — if coverage falls short, lenders will look to strengthen the deal. Common fixes include seller carryback financing, additional equity injection, or bringing in an investor partner.

From term sheet to loan commitment: valuation, timing, and what to expect

Photo by Sebastian Herrmann on Unsplash

Once the term sheet is signed, the lender begins the process toward a full loan commitment. For transactions over $250,000, lenders will usually commission a third-party business valuation. Expect to provide additional documentation and sign multiple forms.

Typical timing:

- 25–45 days to receive a loan commitment (varies by lender and workload)

- Another 15–30+ days to clear closing conditions and fund — total process often averages 50–70 days

If real estate is involved, or if there are construction or insurance requirements, the process can take longer. Conversely, straightforward business acquisitions without real estate can close in about 60 days and, in some cases, as quickly as 30 days. Franchise startups with prepared packages have closed in roughly three weeks in some situations.

Factors that slow down closings (and how to avoid them)

Photo by Sebastian Herrmann on Unsplash

Common causes of delay include:

- Real estate underwriting, appraisals, and title work

- Construction or renovation requiring contractor bids and permits

- Slow responses to lender requests for documents

- Complex ownership structures or messy seller records

To minimize delays: request the seller’s tax returns early, gather your personal documents beforehand, and work with a broker or advisor who can flag weaknesses ahead of time and present a clean package to lenders.

The role of a middleman (broker/advisor) in SBA acquisition financing

My role as an advisor is to act as the middleman between you and the lending market. I help:

- Assemble and review your package

- Spot and correct deal weaknesses

- Prepare a credit memo to present to probable lenders

- Shop the deal across banks, credit unions, and non-bank SBA lenders

In most cases I’m not charging you an upfront fee — I receive a referral fee from the lending institution when the deal closes. Having an experienced facilitator on your side can significantly increase the likelihood of a clean, timely closing.

Collateral, equity injection, and liquidity: what lenders expect

Key underwriting expectations:

- Equity injection: typically 10% of purchase price

- Post-close liquidity: generally an additional ~10% held as working capital after close

- Collateral: loans over $500,000 often require additional collateral if there's a collateral shortfall — lenders may seek a second lien on primary or rental real estate

Loans under $500,000 generally do not require additional collateral beyond the business assets, although some banks may attempt to request it. If liquidity is tight you have options: seller financing, bringing in an investor partner (often under 20% ownership to preserve borrowing profile), or negotiating different deal terms.

Practical deal-structuring tips and quick fixes

If your deal is close but not quite there, consider these practical tactics:

- Ask for seller carryback financing to bridge a DSCR gap

- Bring in a passive investor to increase equity and post-close liquidity

- Structure part of the equity injection as standby seller financing

- Negotiate price or payment terms to make cash flows compute

These options can turn a borderline deal into one that clears underwriting hurdles. The key is transparency and presenting a clean structure to the lender early.

How I can help: next steps and resources

If you're actively pursuing a business purchase, schedule a call so we can:

- Quickly review the seller documents you’ve obtained

- Identify gaps and potential lender objections

- Create a roadmap for a clean, fundable loan package

Visit bookwithbeau.com to schedule a call or sign up for targeted listings at franchiseresallistings.com if you want a curated search for franchise resales. As a Business Ownership Coach | Investor Financing Podcast host, my goal is to move you from browsing listings to closing with confidence.

“Get the past three years of tax returns… we underwrite off the tax returns.” — Practical, blunt advice: documentation matters.

Conclusion: how to move forward with confidence

Acquiring a business with SBA financing is a very achievable goal when you come prepared. The most common reason deals slow or fail is missing or messy documentation — so get the seller’s tax returns, assemble your personal financials, and have a clear purchase price and terms ready. Use seller financing, investors, or adjusted structures when necessary to shore up coverage ratios.

As your Business Ownership Coach | Investor Financing Podcast advisor, I’ll help you package the deal, anticipate lender questions, and get you to a term sheet and full loan commitment as efficiently as possible. If you’re ready to take the next step, schedule a call and let’s review your deal.