I'm Beau Eckstein, Business Ownership Coach | Investor Financing Podcast host, and in this post I'm going to walk you through a real-world playbook I used to close a $10 million business acquisition after two large SBA lenders declined to fund the full deal. As a Business Ownership Coach | Investor Financing Podcast voice, I believe the difference between a stalled transaction and a closed acquisition often comes down to deal packaging, lender selection, and timing. Read on for the exact structure, the numbers, and the strategic thinking that made this deal happen.

Quick Snapshot: The Opportunity and the Challenge

The company we acquired is a niche B2B metals-processing service provider serving professional clients across the U.S. and Canada. It had grown rapidly to roughly $50 million in annual revenue with attractive margins and clear runway for expansion. The buyer was ready, but two large SBA lenders failed to approve the full loan proceeds needed to both close the acquisition and leave sufficient working capital for a smooth transition.

As a Business Ownership Coach | Investor Financing Podcast resource, my view is simple: good companies deserve well-structured financing. The goal was to close the deal using conventional and SBA financing without mezzanine debt, and preserve working capital so operations could scale immediately post-close.

Why the First Two SBA Lenders Said No

SBA lenders review risk differently, and for large acquisitions there are often sticking points: perceived leverage, working capital shortfalls, or lender appetite for industry concentration. In this case, the lenders approved partial components but were unwilling to greenlight the full capital stack with adequate working capital left over for the buyer to run the business effectively.

When standard lenders say no, many buyers assume the deal is dead. But experience as a Business Ownership Coach | Investor Financing Podcast host has taught me that “no” often just means you need a smarter structure and a lender package that speaks to underwriting priorities.

How We Moved Fast: From Introduction to Proposal in 10 Business Days

When the buyer was introduced to my team, we were on the clock. Time kills deals, so we prioritized speed without sacrificing precision. Within 10 business days we delivered a complete, lender-ready loan proposal: a capital stack that addressed closing funds, preserved working capital, and avoided risky mezzanine structures.

This rapid turnaround is possible when you know the right lenders to call, what documentation they value, and how to present covenants and cashflow projections in a way that underwriters can quickly assess. As your Business Ownership Coach | Investor Financing Podcast resource, I still emphasize that fast packaging must be accurate—rushed errors create bigger delays downstream.

Deal Structure: The Capital Stack That Closed the Deal

Here’s the play we used—simple, powerful, and aligned with lender underwriting:

- $5,000,000 SBA 7(a) — 10-year term, prime + 1.5%, fully amortized. This provided the core purchase financing and favorable SBA pricing and terms.

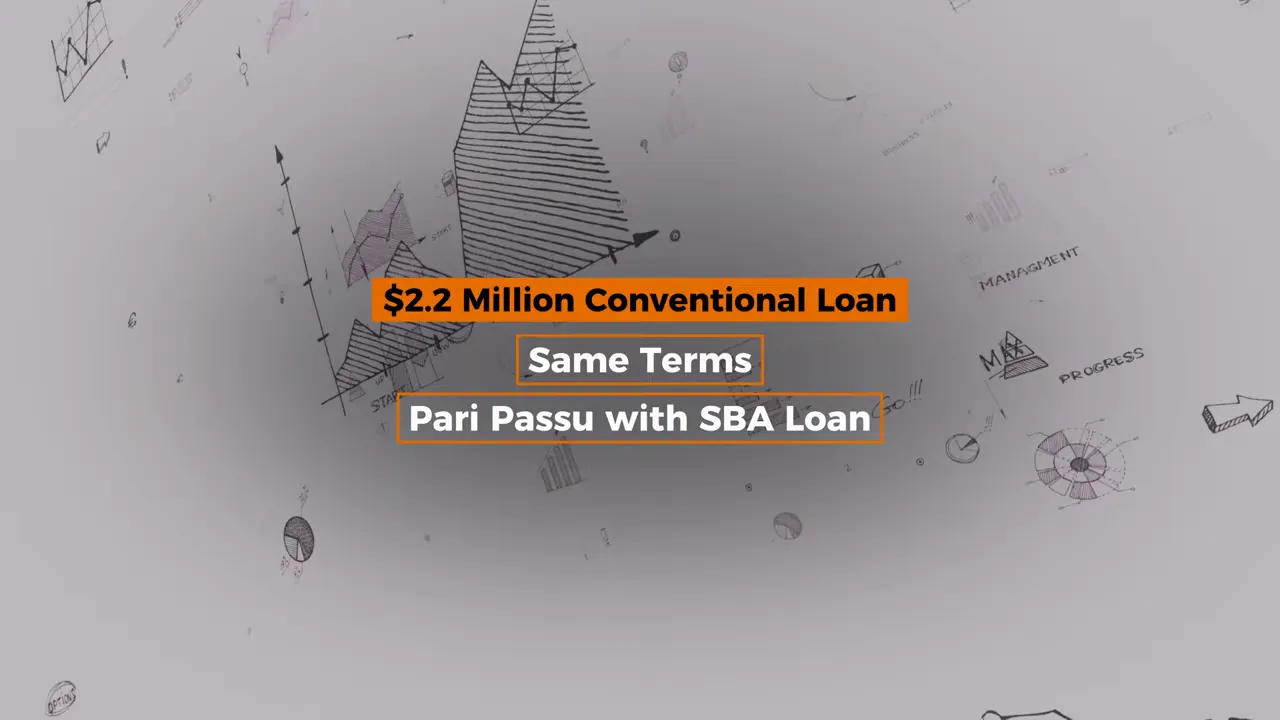

- $2,200,000 Conventional Loan — Same pricing, closed pari passu with the SBA loan. This preserved lender parity while allowing additional leverage beyond the SBA cap on multiple loans.

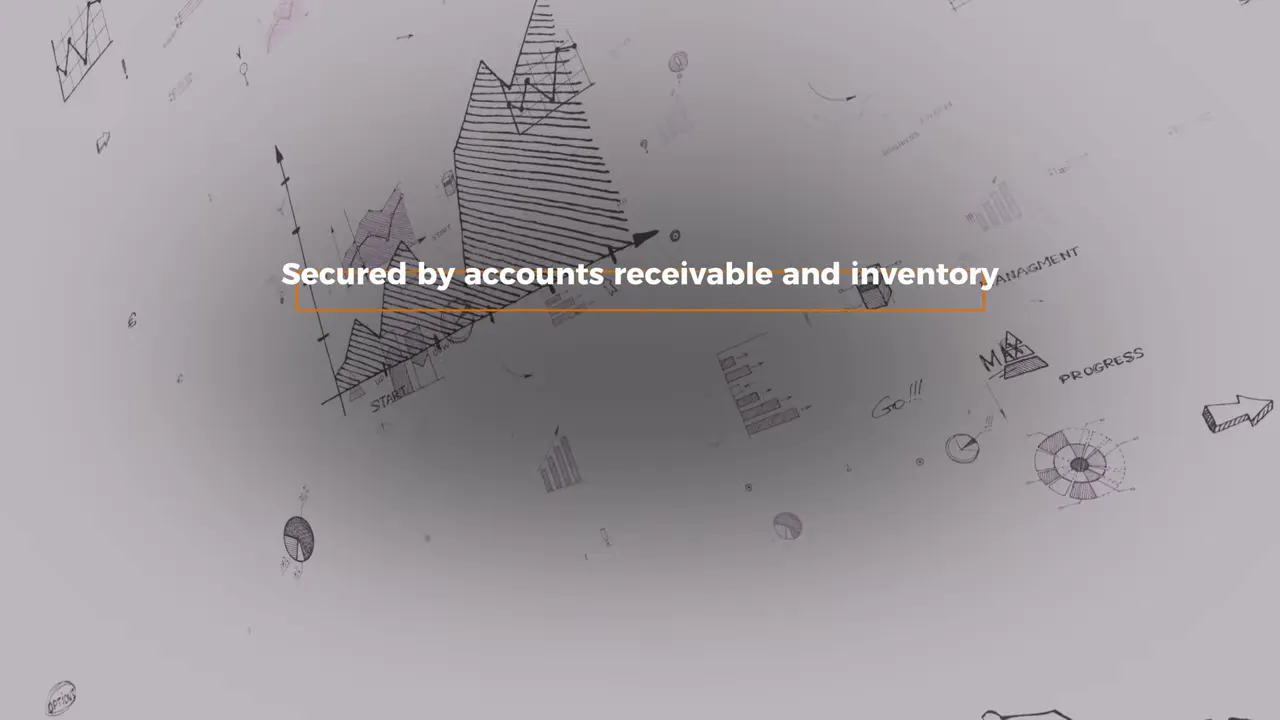

- $780,000 Revolving Line of Credit (LOC) — Secured by accounts receivable and inventory, interest-only payments when drawn. Crucial for immediate operating liquidity post-close.

The result: no mezzanine debt, no dilutive outside investors, and full working capital available. That’s the kind of clean capital stack that allows an acquirer to hit the ground running.

Equity Injection: Smart, Simple, and Small

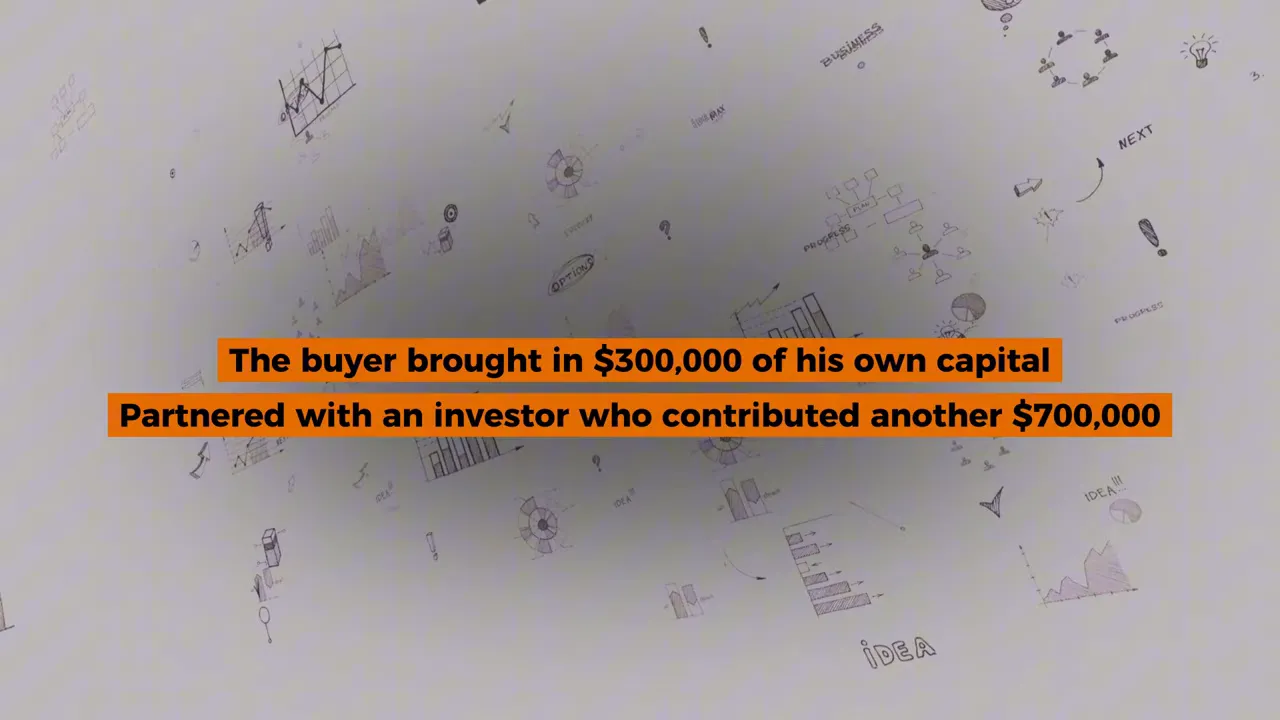

The buyer provided $300,000 of his own capital and partnered with an investor who provided $700,000 in exchange for equity—together meeting the 10% equity injection requirement. This $1M equity made the balance sheet palatable to lenders and bridged the gap without resorting to expensive mezzanine debt or seller notes with tight covenants.

As a Business Ownership Coach | Investor Financing Podcast host, I often recommend that buyers think creatively about equity sources: friend-and-family, strategic partners, or minority co-investors who understand the business. The goal is to secure the right amount of aligned capital while maintaining control and preserving upside.

Working Capital: Why the Revolving LOC Was a Game Changer

One reason the prior lenders backed away was the lack of adequate working capital after closing. By securing a $780,000 revolving line of credit against accounts receivable and inventory, we left the buyer operationally flexible. Interest is paid only when funds are drawn, so the facility acts as true working capital rather than an immediate cash drain.

For buyers, this distinction matters. A balance sheet with sufficient liquidity reduces the operational risk lenders see and enables investments in procurement, sales, and integration that drive post-closing growth.

How a Great Broker Made the Difference

Deals don’t close on numbers alone. The right team wins. A strong loan broker understands how to package financials, which lenders to approach, and how to navigate underwriting nuances. Most borrowers walk into a local bank with paperwork and hope for the best. That’s rarely sufficient for complex, large acquisitions.

As your Business Ownership Coach | Investor Financing Podcast advisor, I regularly help buyers present a lender-friendly narrative: clean recasting of EBITDA, conservative pro formas, clear collateral descriptions, and an orderly equity plan. Those elements reduce surprise requests from lenders and speed approvals.

Lessons and a Playbook You Can Use

Here are the actionable takeaways I want you to remember from this deal:

- Don’t accept the first “no.” Often a different lender or a different structure will work.

- Package the deal for speed: clean financials, clear uses of proceeds, and well-documented collateral.

- Use SBA 7(a) where appropriate, but combine with conventional lending for flexibility.

- Provide real working capital—ideally via a revolving line of credit secured by AR and inventory.

- Keep equity reasonable and aligned: a focused $1M injection in this case preserved control and satisfied lenders.

If you want help applying these lessons to your acquisition, reach out. As a Business Ownership Coach | Investor Financing Podcast resource, I’ve structured dozens of mergers and acquisitions—many that looked dead on arrival until we rethought the capital stack.

Closing Thoughts and Next Steps

The acquisition closed fully funded. The buyer now has $780,000 in working capital, a clean capital structure with no mezzanine debt, and a clear path to scale. That’s what good financing can do.

If you’re considering a purchase or need to rework financing for a stalled deal, get in touch. As a Business Ownership Coach | Investor Financing Podcast host, my focus is on practical, lender-friendly solutions that close deals without unnecessarily diluting equity or adding risky debt.

Ready to talk? Book a call or visit sbaperrypassive.com to start the conversation. If this breakdown helped you, leave a comment and subscribe so I can share more actionable deal strategies.