When it comes to acquiring a business that includes real estate, the way you structure your financing can make a huge difference. In this guide, we’ll dive into the nuances of SBA 7(a) and 504 loans, helping you decide which option might be best for your unique situation. We'll explore purchase price considerations, advantages of each loan type, occupancy requirements, and underwriting processes. Let’s get started!

Purchase Price Considerations

The first thing to analyze in any business acquisition involving real estate is the purchase price of both the business and the real estate itself. This distinction is crucial because it influences the structure of your deal. If the business has a higher purchase price compared to the real estate, you have several options to consider.

If the real estate value is predominant, opting for the SBA 504 loan may be the most logical choice, especially if you are looking for long-term debt. The 504 loan is designed for real estate purchases and can provide you with favorable terms. However, if the business purchase price is greater, you might consider using an SBA 504 loan for the real estate and an SBA 7(a) loan for the business acquisition.

Advantages of SBA 7(a) Loans

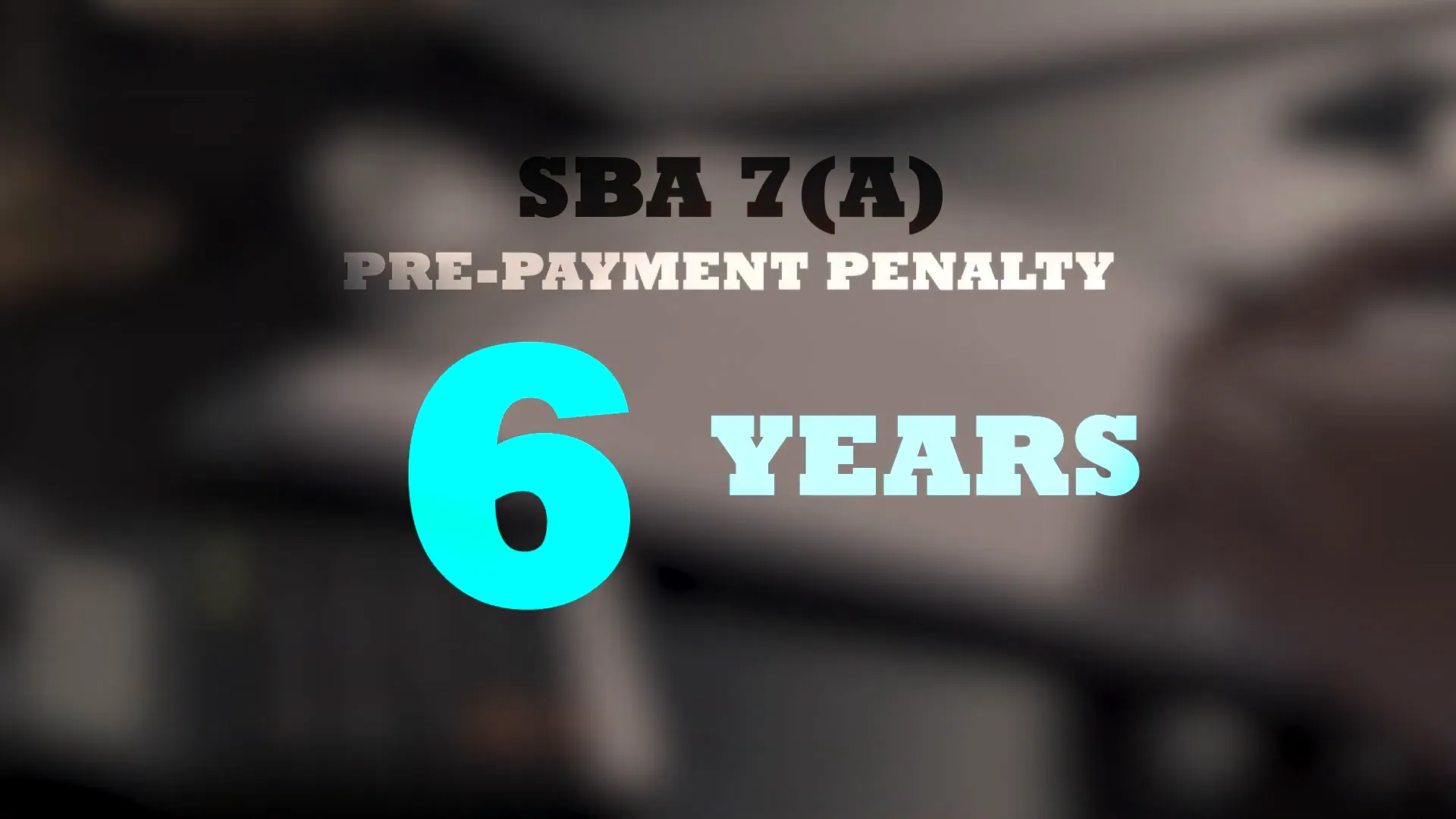

The SBA 7(a) loan program offers several advantages that can be particularly beneficial for business acquisitions. One of the major benefits is the shorter prepayment penalty period, which is typically only three years compared to the ten-year prepayment penalty of the 504 loan. This flexibility is crucial if you plan on expanding or selling the business sooner rather than later.

Additionally, with the 7(a) loan, you can break the financing into two notes. This means you can have one note for the business acquisition and another for the real estate component, amortized over 25 years. This structure helps to minimize your monthly debt payments, allowing for better cash flow management.

Benefits of SBA 504 Loans

On the other hand, if the majority of your purchase price is allocated to real estate, the SBA 504 loan could be the better option. The 504 loan has a two-part structure: a first mortgage through a bank or credit union and a second mortgage guaranteed by the SBA. This loan type provides long-term fixed rates, currently hovering around 6.3%, which is attractive for those looking to stabilize their payments over time.

Moreover, with a 504 loan, you can finance larger transactions, making it a solid choice for more significant business acquisitions. However, it does involve a more complicated underwriting process since both the bank and a Certified Development Company (CDC) must approve the loan.

Occupancy Requirements

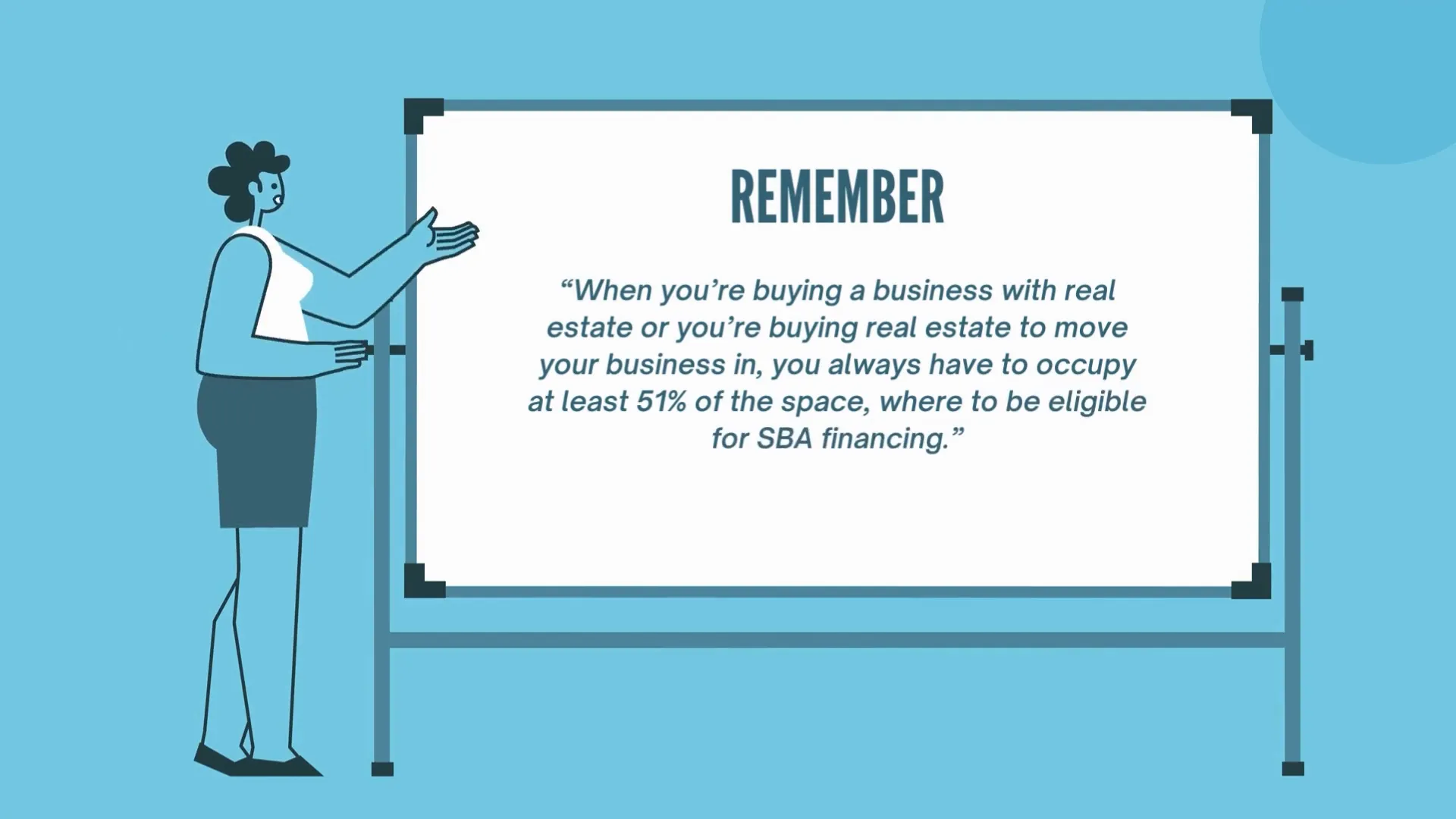

When acquiring a business with a real estate component, it's essential to understand the occupancy requirements set by the SBA. For your financing to be eligible, you must occupy at least 51% of the space. This requirement emphasizes the SBA's focus on ensuring that the loans are used primarily for business operations rather than purely investment purposes.

Underwriting Processes

The underwriting processes for SBA loans differ significantly between the 7(a) and 504 programs. With the SBA 7(a) loan, there is typically only one underwriting process. If you work directly with a Preferred Lender Program (PLP) lender, they can underwrite the loan in-house, streamlining the approval process.

In contrast, the SBA 504 loan requires two underwriting processes. The first is through the bank, while the second is through the CDC, which packages the loan for submission to the SBA. This two-step process can be more time-consuming, but it allows for larger financing amounts.

Refinancing Tips

In today's market, if you already have an SBA loan with a variable rate, it might be an excellent time to consider refinancing. By obtaining a lower margin and extending the term by another 10 years, you can significantly reduce your monthly payments, allowing your business to allocate funds more effectively.

Conclusion

In conclusion, choosing between an SBA 7(a) and a 504 loan for business acquisitions with a real estate component largely depends on the purchase price dynamics and your long-term business goals. Whether you prioritize flexibility with the 7(a) or the stability of the 504, understanding the intricacies of each option is crucial for making informed decisions.

If you’re ready to explore your options further, consider booking a strategy call to discuss your specific situation and find the best financing solution for your business acquisition needs. Remember, the right financing can unlock the potential of your business and set you on the path to success.

About Beau Eckstein

Beau Eckstein is a seasoned business ownership coach and financing expert. With over 20 years in the lending industry, Beau specializes in helping entrepreneurs navigate the complexities of business acquisition financing, providing tailored strategies for success.

For additional insights and guidance on SBA financing, be sure to check out the Business Ownership Academy and consider booking a consultation with Beau to discuss your unique business aspirations.