Business Ownership Coach | Investor Financing Podcast is delivering a timely opportunity: SBA rates have eased, and that opens a window for business owners to lock in long-term, low-cost financing for owner-occupied commercial real estate, expansions, construction, and refinances. If you are thinking about buying a building or expanding operations, this is one of those moments where the math can create long-term wealth.

Why the recent rate drop matters

Photo by Şahin Sezer Dinçer on Unsplash

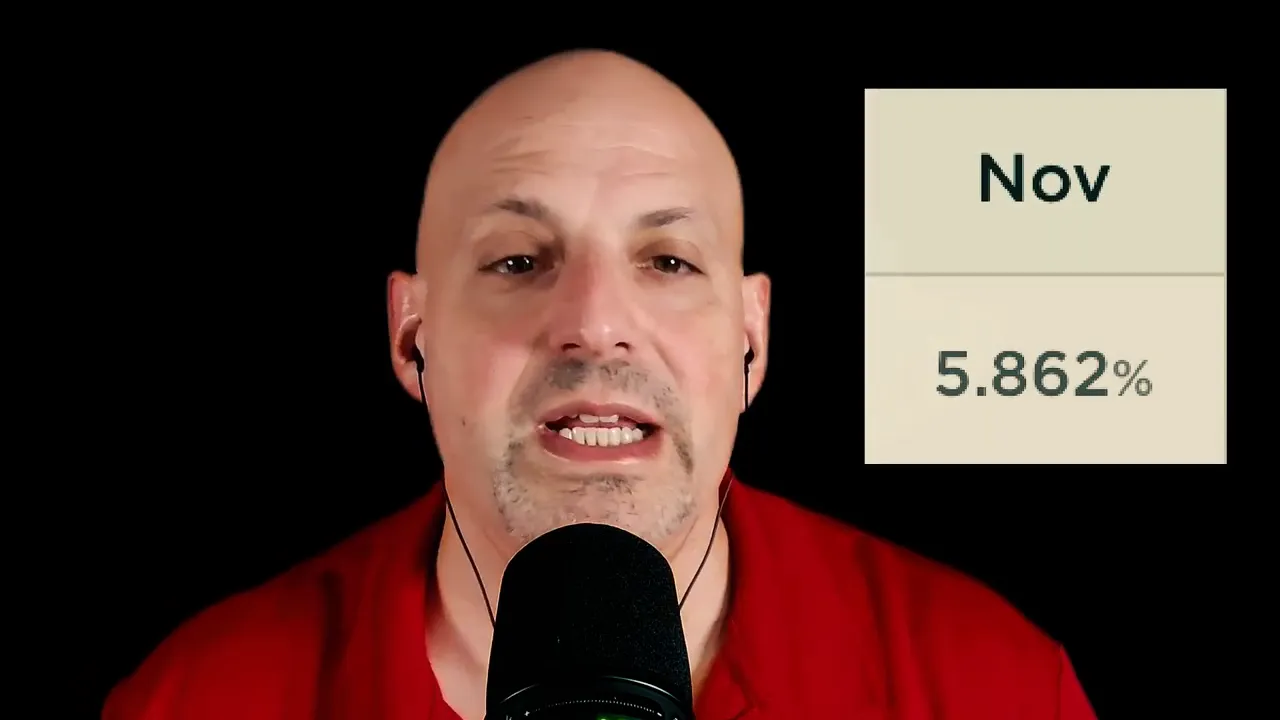

Today the SBA 504 25-year debenture rate sits at 5.86% (about 20 basis points lower for manufacturing businesses). That fixed second-position rate becomes a powerful tool when paired with a negotiated first mortgage from a bank. Low fixed rates mean predictable debt service for the next 25 years, which can dramatically improve cash flow projections and return-on-equity for owner-occupied properties.

Why act now? Falling rates create opportunities to acquire properties where sellers or lenders may be under pressure, to refinance existing debt to lower payments, or to fund renovations and ground-up construction with favorable long-term financing. With Wall Street Journal Prime trending down toward 7.25%, financing environments are shifting in favor of buyers who move decisively.

Understanding SBA 504: structure and benefits

The SBA 504 program is a two‑piece financing structure:

- First mortgage (senior debt) — Provided by a bank or lender and negotiated at market levels.

- Second mortgage (CDC debenture) — The SBA guaranteed piece, typically a fixed 25-year debenture at the published rate (currently 5.86%).

This blend often produces a much lower blended cost of capital than straight conventional financing. The 504 excels for owner-occupied commercial real estate purchases and construction projects where long-term fixed rates are a priority. It also allows for refinancing in many cases, giving owners flexibility to reduce monthly obligations and improve cash-on-cash returns.

SBA 504 vs SBA 7(a): when each makes sense

Two common SBA options—504 and 7(a)—serve different needs:

- SBA 504 — Best when you want a long-term fixed rate for real estate, especially purchases and long-term construction financing. Typically capped at 90% total financing on expansions, but yields a superior blended rate in many transactions.

- SBA 7(a) — More flexible for a wider set of business uses, including working capital and renovations. The 7(a) can potentially provide 100% financing on expansions and follows a single underwriting process, which can simplify approvals for complex value-add plays.

In practice, choose the 504 when stable, long-term fixed financing on property matters most. Choose the 7(a) when you need underwriting simplicity or the ability to finance a higher percentage of the project cost. Sometimes a combined strategy or a side-by-side comparison reveals the best outcome, depending on business cash flow, collateral, and growth plans.

Occupancy rules and construction requirements

Photo by Jakub Żerdzicki on Unsplash

SBA programs have specific occupancy rules that affect eligibility:

- For existing buildings, the borrower must occupy at least 51% of the property to qualify as owner-occupied real estate.

- For ground-up construction, initial occupancy requirements are higher: at least 60% of the square footage must be owner-occupied from day one, rising to 80% within two years.

These thresholds matter for planning acquisition structures. If you intend to lease portions to third parties, ensure your occupancy percentages align with SBA rules. Proper planning at underwriting avoids surprises and preserves the benefits of the SBA-backed rates.

What types of projects and businesses qualify

SBA programs can finance a wide range of projects and industries. Common examples include:

- Hospitality projects

- Gas stations and convenience stores

- Bowling alleys, fitness centers, and other commercial facilities

- Franchise acquisitions and owner-occupied commercial properties

There are a few ineligible or restricted industries under SBA rules, but most operating businesses—especially those that can demonstrate stable cash flow and meet size standards—qualify. The best way to confirm is to run the specifics through an experienced SBA adviser who knows the nuances between lenders and programs.

How to evaluate your options and move forward

Photo by Jakub Żerdzicki on Unsplash

Making the most of lower SBA rates requires two things: clarity and speed. Start by mapping the scope of your project, including purchase price, renovation budget, occupancy plans, and projected cash flow. Then:

- Compare 504 and 7(a) structures side by side to calculate blended rates and payment schedules.

- Confirm occupancy percentages and timing for construction projects.

- Ask lenders for term sheets and run pro forma scenarios showing debt service and cash-on-cash returns.

Tip: For expansions, the 7(a) can sometimes offer up to 100% financing, eliminating the need for large equity injections. For long-term stability on real estate debt, the 504’s 25-year fixed debenture is hard to beat.

Practical next steps and consultation

Photo by Jakub Żerdzicki on Unsplash

If you are evaluating an acquisition, construction, or refinance, a short planning call with a seasoned advisor can crystallize the best path forward. A strategic conversation will uncover whether the 504 or 7(a) better suits your goals, which lenders are most competitive for your industry, and how to structure the deal to maximize long-term wealth creation.

Remember: lower rates create windows of opportunity. Treat these moments as tactical chances to improve capital structure, reduce monthly obligations, and set your business up for predictable growth.

Quick checklist before you apply

- Confirm occupancy percentage aligns with SBA rules

- Assemble realistic cash flow projections and rent schedules

- Gather historical financials and a clear business plan for the project

- Compare blended rates and total cost of capital across 504 and 7(a)

- Evaluate lender relationships and experience with SBA products

Final thoughts

Photo by Jakub Żerdzicki on Unsplash

Lower SBA debenture rates combined with a falling prime environment create a rare, impactful opportunity for business owners and investors. Whether the goal is buying a building, refinancing to reduce payments, or funding construction, understanding the differences between SBA 504 and 7(a) is essential to designing the most effective financing solution.

Business Ownership Coach | Investor Financing Podcast strategies focus on structuring deals that protect cash flow while building long-term equity in real estate and business assets. If you are ready to explore options, get the numbers together and consult with a knowledgeable SBA advisor who can walk through scenarios and produce an actionable plan.