I'm Beau Eckstein, and if you've been following my work as Business Ownership Coach | Investor Financing Podcast, you already know that the first true test in buying a business with an SBA loan is getting the paperwork right. In this article I walk you through every document you need for an SBA business acquisition loan, including the often-forgotten items, and I break down SBA Form 413—the personal financial statement—step by step so your application moves smoothly.

If you’re serious about buying a business, I created this guide to save you time and prevent costly delays. Whether you’ve never filled out an SBA form before or you’ve been through the process and want a cleaner, faster experience, you’ll find practical, lender-ready advice here from your Business Ownership Coach | Investor Financing Podcast.

Photo by Sollange Brenis on Unsplash

What Lenders Look For: The Big Picture

When you apply for an SBA 7(a) or 504 loan to buy a business, lenders want to run a very specific set of numbers. Their primary question is simple: can this business support the new debt? To answer that, they need complete, accurate documentation from both you and the seller so they can calculate debt service coverage and evaluate risk.

Providing a complete file up front shows lenders you’re organized and reduces the back-and-forth that slows approvals. As your Business Ownership Coach | Investor Financing Podcast, I recommend preparing the full set of documents before you submit anything. That gives you the best shot at a fast, clean approval.

Document Checklist: Everything You Need (Buyer & Seller)

Below is the practical checklist lenders expect for an SBA business acquisition file. Getting each item together before your lender asks will make you stand out:

- Recent personal bank statements (typically 3–6 months)

- Investment and retirement account statements

- Recent personal tax returns and pay stubs

- Mortgage statements, auto loan statements, credit card balances

- Details on any personal real estate or high-value personal property

- Seller-provided business financials: tax returns, profit & loss, balance sheets, interim statements

- Asset list for the business (FF&E, inventory; the seller should provide)

- Purchase agreement or letter of intent

- Any lease or real estate documents tied to the business

- Copies of licenses, contracts, or material agreements

Notice one important distinction: you do not put the business’s assets on your personal financial statement. You list the value of your ownership interest as one line item on the personal form, and the business’s assets and liabilities live on the business financials. Keeping that separation clean prevents confusion and credibility issues with lenders.

SBA Form 413: What It Is and Why It Matters

SBA Form 413 is the personal financial statement the SBA requires for most 7(a) and 504 loans. It’s a snapshot of your personal net worth, debts, and contingent liabilities. Lenders use it to verify your personal capacity and to uncover obligations that could affect your ability to guarantee the loan.

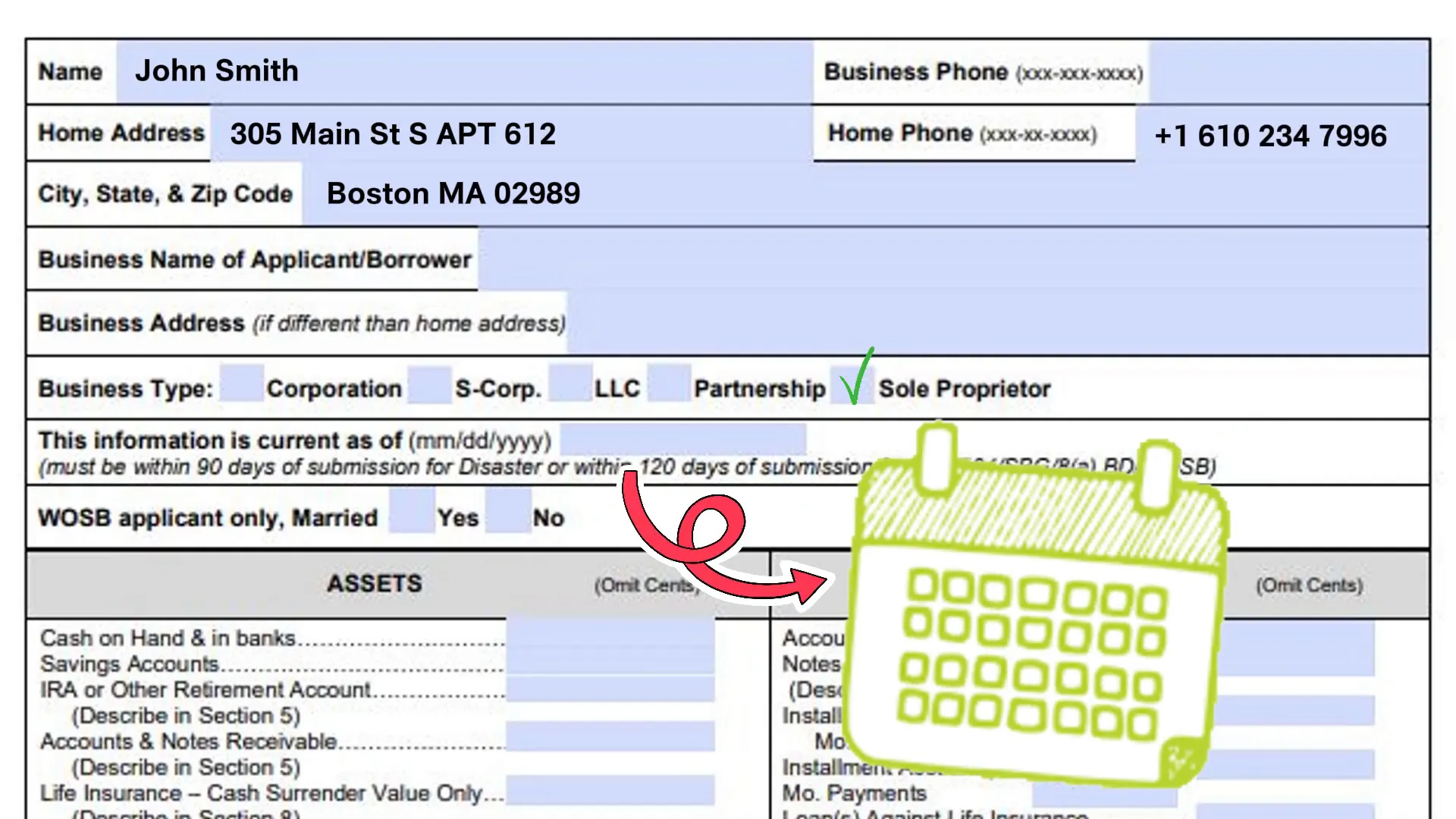

Download the latest version directly from sba.gov. As of February 13, 2025, lenders expect the current form—using an outdated PDF can create unnecessary delays. The form asks for:

- Program selection (7(a), 504, or other)

- Personal identifying information and the date the statement is current

- All personal assets (cash, accounts, investments, retirement, personal real estate, vehicles, and the value of any business ownership)

- All personal liabilities (mortgages, vehicle loans, credit cards, lines of credit, other personal loans)

- Annual income detail and contingent liabilities (co-signs, pending legal obligations)

Complete accuracy matters. Lenders will pull your credit and reconcile what you list against what they find. Omissions or significant discrepancies can raise red flags and lengthen underwriting.

Step-by-Step: How to Complete Form 413 Correctly

Follow these practical steps when filling out Form 413:

- Download the latest form from sba.gov.

- Gather supporting documents: bank statements, investment and retirement statements, mortgage and auto loan statements, recent tax returns, pay stubs, property tax records or appraisals, and credit card statements.

- At the top of the form, select the correct SBA program and enter the date the information is current.

- List personal assets on the left column—cash, checking/savings, stocks/bonds, retirement accounts, personal real estate (use verifiable values), vehicles, and the value of any business ownership you personally hold.

- List personal liabilities on the right—mortgages, car loans, credit cards, lines of credit, and other debts. Be precise: lenders will find what you omit when they pull your credit report.

- Enter total annual income—salary, bonuses, rental income, dividends, other income sources.

- Disclose contingent liabilities—co-signed loans, pending lawsuits, guarantees, and any other obligations you might be responsible for.

- Sign and date. Use the fillable PDF version if possible to keep your math readable and neat.

Remember: if you are married, your spouse must be included on the form, even if they are not applying for the loan. This is a common surprise for many applicants, so plan ahead.

As your Business Ownership Coach | Investor Financing Podcast, I recommend documenting every value you list with a supporting statement or appraisal so lenders can verify the numbers quickly.

Common Mistakes That Delay Approval—and How to Avoid Them

Here are the frequent errors I see—and how to prevent them:

- Leaving sections blank: If something doesn't apply, write “NA.” Blank fields make lenders think you missed something.

- Mixing business assets with personal assets: List only personal assets on Form 413. Business assets belong on the business financial statements.

- Guessing values for real estate or investments: Use recent statements, appraisals, or property tax records. Verifiable numbers prevent delays.

- Forgetting to list all debts (especially co-signed loans): Lenders will find them on your credit report; list them upfront.

- Poor math or unsigned forms: Double-check totals and sign and date the form before submitting.

Fix these issues before you submit and you’ll avoid weeks of unnecessary follow-up. A clean Form 413 communicates credibility and readiness.

Why Working with an SBA Loan Broker Speeds Things Up

Choosing the right lender can make or break your deal. A good SBA loan broker knows which lenders are approving deals like yours right now, their approval criteria, and how to package applications so they get priority in underwriting.

Working with a broker helps in three ways:

- Lender matching: We know who’s funding what—so you avoid wasting time with lenders that aren’t a fit.

- File packaging: Brokers assemble the file to highlight strengths and minimize red flags, which leads to smoother reviews and better terms.

- Negotiation and follow-up: We handle lender questions and negotiate terms so you stay focused on closing the business acquisition.

If you’d like help navigating the lender landscape and speeding your timeline, I invite you to schedule a call at bookwithbeau.com. As Business Ownership Coach | Investor Financing Podcast, my goal is to get your project on the fastest track to closing.

Final Checklist and Next Steps

Before you submit anything, run through this final checklist:

- Download the current SBA Form 413 from sba.gov (verify the date).

- Gather 3–6 months of bank statements, investment/retirement statements, and current mortgage/auto statements.

- Collect personal tax returns and proof of income (pay stubs) for the most recent period.

- Get seller-provided business financials (tax returns, P&Ls, balance sheets, interim statements).

- Confirm the value of any personal real estate with recent appraisals or tax records.

- List all personal liabilities, including co-signed loans or contingent obligations.

- Sign and date Form 413 and use the fillable PDF for readability.

When your file is complete, you’ll be in a great position to present it to lenders or bring it to a broker who can shop it efficiently.

Conclusion: Present Your Best Financial Self

Filling out SBA Form 413 and assembling a complete acquisition loan file can feel daunting, but it’s fundamentally about organization, accuracy, and transparency. Make sure you use the current form, document every value, separate personal and business assets, disclose all liabilities, and always sign and date your forms.

If you want help getting this done right the first time, schedule a call at bookwithbeau.com—I'll walk through your project, match you with the right lender, and help package your file so your deal gets to the top of the lender’s pile. As your Business Ownership Coach | Investor Financing Podcast, I’m focused on practical steps that get you from offer to close.

Prepare the documentation, complete Form 413 carefully, and present your best financial self—doing that will dramatically increase your odds of a smooth SBA loan approval and a successful acquisition.